Space Militarization Market Driven by Advancements in Military Satellite Technologies

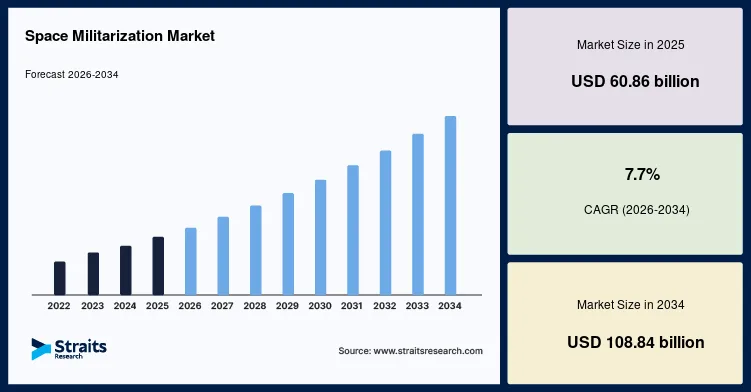

The global space militarization market is witnessing significant growth as governments worldwide increase investments in orbital defense capabilities to strengthen national security and strategic deterrence. The market was valued at USD 60.86 billion in 2025 and is projected to reach USD 108.84 billion by 2034, growing at a CAGR of 7.7% during the forecast period. Rising investments in defense satellite infrastructure, anti-satellite (ASAT) weapon systems, space-based intelligence networks, and advanced surveillance technologies are driving the expansion of the global market.

Space has become a critical strategic domain for military operations, enabling secure communications, navigation, intelligence gathering, missile warning, and battlefield coordination. Nations are increasingly prioritizing the development of resilient space defense architectures to protect critical satellite assets while enhancing situational awareness and operational readiness. Continuous advancements in satellite technologies, space surveillance systems, and defense modernization programs are expected to support long-term market growth.

For detailed market insights, growth forecasts, and competitive analysis, visit:

https://straitsresearch.com/report/space-militarization-market

Market Drivers

Rising Investment in Defense Satellite Infrastructure

One of the primary drivers of the space militarization market is the increasing investment in military satellite infrastructure. Governments are deploying advanced communication, navigation, reconnaissance, and early-warning satellites to improve operational efficiency and strengthen national security.

Military satellites provide secure communications, real-time intelligence, and surveillance capabilities that are essential for modern defense operations. As geopolitical tensions continue to evolve, countries are expanding satellite constellations to improve strategic resilience.

Growing Development of Anti-Satellite (ASAT) Capabilities

The development of anti-satellite weapon systems has become a major focus for defense agencies worldwide. Nations are investing in technologies capable of protecting critical space assets while enhancing deterrence against potential adversaries.

Advancements in kinetic and non-kinetic ASAT systems, electronic warfare technologies, and cyber defense capabilities continue to shape the competitive landscape of the global space militarization market.

Increasing Demand for Space-Based Intelligence

Modern military operations increasingly depend on space-based intelligence, surveillance, and reconnaissance (ISR) systems. High-resolution imaging satellites, electronic intelligence platforms, and synthetic aperture radar satellites provide critical information for mission planning and battlefield awareness.

Growing investments in real-time data collection and secure military communications are accelerating the adoption of advanced space-based intelligence systems.

Defense Modernization Programs

Governments around the world continue to implement comprehensive defense modernization initiatives aimed at strengthening space security. Rising defense budgets and the establishment of dedicated space military organizations are encouraging investments in advanced orbital defense technologies, satellite resilience, and integrated command systems.

Market Challenges

High Development Costs

Developing and deploying military satellites, launch systems, and space defense technologies requires substantial financial investment. Research, development, testing, and long-term operational maintenance significantly increase program costs for defense organizations.

Space Debris and Orbital Congestion

The increasing number of satellites and space missions has contributed to growing orbital congestion and space debris. These challenges increase the risk of satellite collisions and require continuous investment in space situational awareness and debris monitoring technologies.

International Regulatory Concerns

The militarization of space raises complex legal and diplomatic challenges. International treaties, evolving space governance frameworks, and geopolitical considerations influence defense strategies and may affect future military space programs.

Market Segmentation

By Platform

The space militarization market is segmented into satellites, launch vehicles, ground stations, and supporting infrastructure.

Satellites account for the largest market share due to their critical role in military communications, intelligence gathering, navigation, missile warning, and surveillance operations. Governments continue to invest heavily in next-generation satellite constellations capable of operating in contested environments.

Ground stations and command infrastructure are also experiencing significant growth as military organizations modernize space operations and improve data processing capabilities.

By Application

Based on application, the market is segmented into intelligence, surveillance and reconnaissance (ISR), communication, navigation, missile warning, electronic warfare, and others.

Intelligence, surveillance, and reconnaissance represent the largest application segment due to increasing demand for real-time situational awareness and battlefield intelligence. Military organizations rely on advanced space-based ISR systems to monitor global activities and support strategic decision-making.

Secure communication and navigation systems also account for a significant share as modern military operations depend on uninterrupted satellite connectivity.

By End User

The market is segmented into defense agencies, space forces, intelligence organizations, and government institutions.

Defense agencies account for the largest market share as governments continue expanding military space programs and investing in orbital defense capabilities. Dedicated space commands and intelligence organizations are increasingly deploying advanced satellite systems to strengthen national security and improve operational readiness.

Regional Insights

North America

North America dominates the space militarization market due to its substantial defense budget, advanced aerospace industry, and continuous investments in military space technologies. The United States leads the global market through ongoing satellite modernization programs, advanced missile defense systems, and the expansion of dedicated military space operations.

Europe

Europe represents a significant market driven by increasing investments in defense modernization, collaborative space security initiatives, and satellite communication programs. Countries including France, Germany, Italy, and the United Kingdom continue strengthening military space capabilities through strategic partnerships and technological innovation.

Asia-Pacific

Asia-Pacific is expected to register the fastest growth during the forecast period. Rising geopolitical tensions, expanding defense budgets, and increasing investments in indigenous satellite development are driving market expansion across China, India, Japan, South Korea, and Australia.

Governments throughout the region continue to strengthen space surveillance, missile defense, and military communication capabilities.

Latin America, Middle East, and Africa

Latin America and the Middle East & Africa are gradually increasing investments in satellite communications, border surveillance, and defense modernization. Growing regional security concerns and expanding space capabilities are expected to create new opportunities for market participants over the forecast period.

Key Players Analysis

The space militarization market is highly competitive, with leading aerospace and defense companies focusing on satellite technologies, secure communications, missile defense systems, and advanced space surveillance capabilities. Strategic collaborations, defense contracts, and continuous investment in research and development remain central to maintaining technological leadership.

Major companies operating in the space militarization market include:

-

Lockheed Martin Corporation

-

Northrop Grumman Corporation

-

RTX Corporation

-

Boeing Defense, Space & Security

-

L3Harris Technologies Inc.

-

BAE Systems plc

-

Airbus Defence and Space

-

Thales Group

-

Leonardo S.p.A.

-

General Dynamics Corporation

-

Israel Aerospace Industries Ltd.

-

Mitsubishi Electric Corporation

-

Maxar Technologies

-

Rocket Lab USA, Inc.

-

Sierra Space Corporation

Conclusion

The space militarization market is expected to witness sustained growth through 2034, driven by rising investments in military satellite infrastructure, expanding space-based intelligence networks, and increasing development of orbital defense capabilities. Defense modernization programs, technological advancements, and growing geopolitical competition continue to reshape the strategic importance of space as a defense domain. Companies investing in advanced satellite technologies, secure communications, and resilient space systems are well-positioned to capitalize on the growing demand for military space capabilities.

About Us

Straits Research is a leading market research and intelligence organization specializing in research, analytics, and advisory services. The company provides comprehensive market reports, industry insights, and strategic business intelligence across multiple industries, helping organizations identify growth opportunities and make informed business decisions.

Contact Us

Email: [email protected]

Tel: +1 646 905 0080 (U.S.)

Tel: +44 203 695 0070 (U.K.)

0 comments

Log in to leave a comment.

Be the first to comment.