Nanoelectronics Innovation Transforming the High-K and ALD CVD Metal Precursors Market

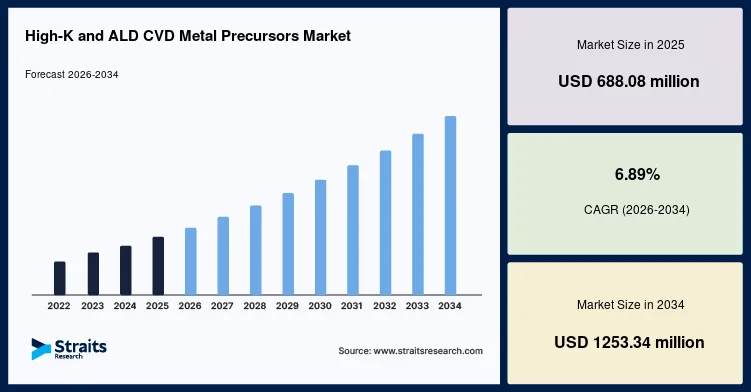

The High-k & ALD/CVD Metal Precursors market is projected to reach USD 1,253.34 million by 2034, growing at a CAGR of 6.89%.

The global high-k and ALD CVD metal precursors market is witnessing significant growth due to increasing semiconductor manufacturing, rising demand for advanced logic and memory chips, expanding adoption of atomic layer deposition (ALD) and chemical vapor deposition (CVD) technologies, and continuous advancements in miniaturized electronic devices. The global high-k and ALD CVD metal precursors market size was valued at USD 688.08 million in 2025 and is projected to grow from USD 735.48 million in 2026 to USD 1,253.34 million by 2034, registering a CAGR of 6.89% during the forecast period (2026–2034).

High-k and ALD CVD metal precursors are specialized chemical compounds used in semiconductor fabrication to deposit ultra-thin, high-performance dielectric and metal films. These materials play a critical role in manufacturing integrated circuits, memory devices, logic chips, sensors, and advanced semiconductor components by enabling precise film deposition at the atomic level. Growing investments in advanced semiconductor manufacturing and next-generation chip technologies continue to drive market expansion.

Market Drivers

Rising Demand for Advanced Semiconductors

Increasing production of high-performance processors, memory chips, and integrated circuits is driving demand for high-quality ALD and CVD metal precursors.

Growth of Consumer Electronics

The expanding market for smartphones, laptops, wearable devices, and consumer electronics is increasing semiconductor fabrication activities worldwide.

Expansion of Artificial Intelligence and High-Performance Computing

Rapid adoption of AI, machine learning, cloud computing, and data centers is accelerating demand for advanced semiconductor devices manufactured using ALD and CVD technologies.

Increasing Adoption of 5g Technology

Growing deployment of 5G infrastructure and connected devices is supporting semiconductor innovation and increasing demand for high-k dielectric materials.

Advancements in Semiconductor Manufacturing

Continuous scaling of semiconductor nodes and transition toward smaller process technologies are boosting the use of precision deposition materials.

For Detailed Insights, Visit:

https://straitsresearch.com/report/high-k-and-ald-cvd-metal-precursors-market

Market Challenges

High Manufacturing Costs

Producing high-purity metal precursors requires sophisticated chemical synthesis processes and stringent quality control, increasing production costs.

Stringent Purity Requirements

Semiconductor manufacturing demands ultra-high-purity materials, making precursor production technically challenging.

Supply Chain Disruptions

Global semiconductor supply chain constraints and raw material shortages may impact precursor availability and production schedules.

Environmental and Safety Regulations

Manufacturers must comply with strict environmental, chemical handling, and workplace safety regulations during production and transportation.

Market Segmentation

The high-k and ALD CVD metal precursors market is segmented based on precursor type, deposition technology, application, and region.

By Precursor Type

The market is categorized into:

Hafnium Precursors

Zirconium Precursors

Titanium Precursors

Aluminum Precursors

Tantalum Precursors

Others

Hafnium precursors account for a significant market share due to their widespread use in high-k dielectric layers for advanced semiconductor devices.

By Deposition Technology

The market includes:

Atomic Layer Deposition (ALD)

Chemical Vapor Deposition (CVD)

Atomic Layer Deposition (ALD) dominates the market owing to its superior precision, conformality, and suitability for advanced semiconductor manufacturing.

By Application

The market is segmented into:

Logic Devices

Memory Devices

Integrated Circuits

MEMS Devices

Sensors

Power Electronics

Others

Memory devices represent a major application segment due to increasing production of DRAM, NAND flash, and next-generation memory technologies.

By Region

The market is analyzed across:

North America

Europe

Asia-Pacific

Latin America

Middle East & Africa

Regional Insights

North America

North America holds a significant share of the high-k and ALD CVD metal precursors market due to strong semiconductor research, advanced chip manufacturing, substantial investments in AI infrastructure, and the presence of leading semiconductor companies.

Europe

Europe represents a major market supported by expanding semiconductor manufacturing initiatives, growing investments in automotive electronics, and increasing research in advanced semiconductor materials.

Asia-Pacific

Asia-Pacific is expected to witness the fastest growth due to the presence of major semiconductor fabrication facilities, increasing electronics manufacturing, expanding foundry capacity, and strong investments in advanced chip production across China, Taiwan, South Korea, Japan, and India.

Latin America

Latin America is experiencing gradual growth driven by expanding electronics manufacturing, increasing industrial automation, and growing semiconductor demand.

Middle East &Amp; Africa

The region is witnessing steady growth owing to increasing digital transformation, government investments in technology infrastructure, and expanding electronics markets.

Technology Trends and Market Opportunities

The high-k and ALD CVD metal precursors market is evolving through innovations in ultra-high-purity precursor chemistry, next-generation ALD processes, advanced semiconductor packaging, 3D NAND technology, gate-all-around (GAA) transistor architectures, and EUV lithography. Manufacturers are increasingly developing customized precursor formulations that improve deposition efficiency, reduce defects, and support advanced semiconductor node fabrication.

Growing investments in artificial intelligence, quantum computing, automotive semiconductors, Internet of Things (IoT), 5G communication infrastructure, and advanced semiconductor fabs are creating significant opportunities for market participants. Furthermore, increasing global investments in domestic semiconductor manufacturing are expected to support long-term market growth.

Key Players Analysis

The high-k and ALD CVD metal precursors market is highly competitive, with leading chemical manufacturers focusing on high-purity precursor development, strategic collaborations, capacity expansion, and semiconductor process innovation.

Major companies operating in the market include:

Merck KGaA

Entegris, Inc.

Air Liquide S.A.

SK Materials Co., Ltd.

Adeka Corporation

UP Chemical Co., Ltd.

Hansol Chemical Co., Ltd.

Strem Chemicals, Inc.

American Elements

Soulbrain Co., Ltd.

These companies continue to invest in advanced precursor chemistry, semiconductor-grade material production, research and development, and strategic partnerships to strengthen their positions in the global high-k and ALD CVD metal precursors market.

Related Report

Semiconductor Chemicals Market

https://straitsresearch.com/report/semiconductor-chemicals-market

About Us

Straits Research is a leading market research and intelligence organization specializing in analytics, advisory services, and comprehensive market research reports across multiple industries.

Contact Us

Email: [email protected]

U.S. Tel: +1 646 905 0080

U.K. Tel: +44 203 695 0070

0 comments

Log in to leave a comment.

Be the first to comment.