5 Different Types of Home Loans in India

Introduction:

In India, owning a home is not just a financial goal but also a cherished dream for many. With the real estate market flourishing, the prospect of buying a home has become increasingly attainable, thanks to the availability of various home loan options.

However, navigating through the maze of home loan types can be overwhelming for prospective buyers. To simplify this process and empower you with knowledge, let's delve into the five different types of home loans prevalent in India.

Looking to secure your dream home with the right loan? Our expert team specializes in guiding you through the diverse landscape of home loans services. Whether you prefer stability, flexibility, or competitive rates, we're here to help you find the perfect fit.

-

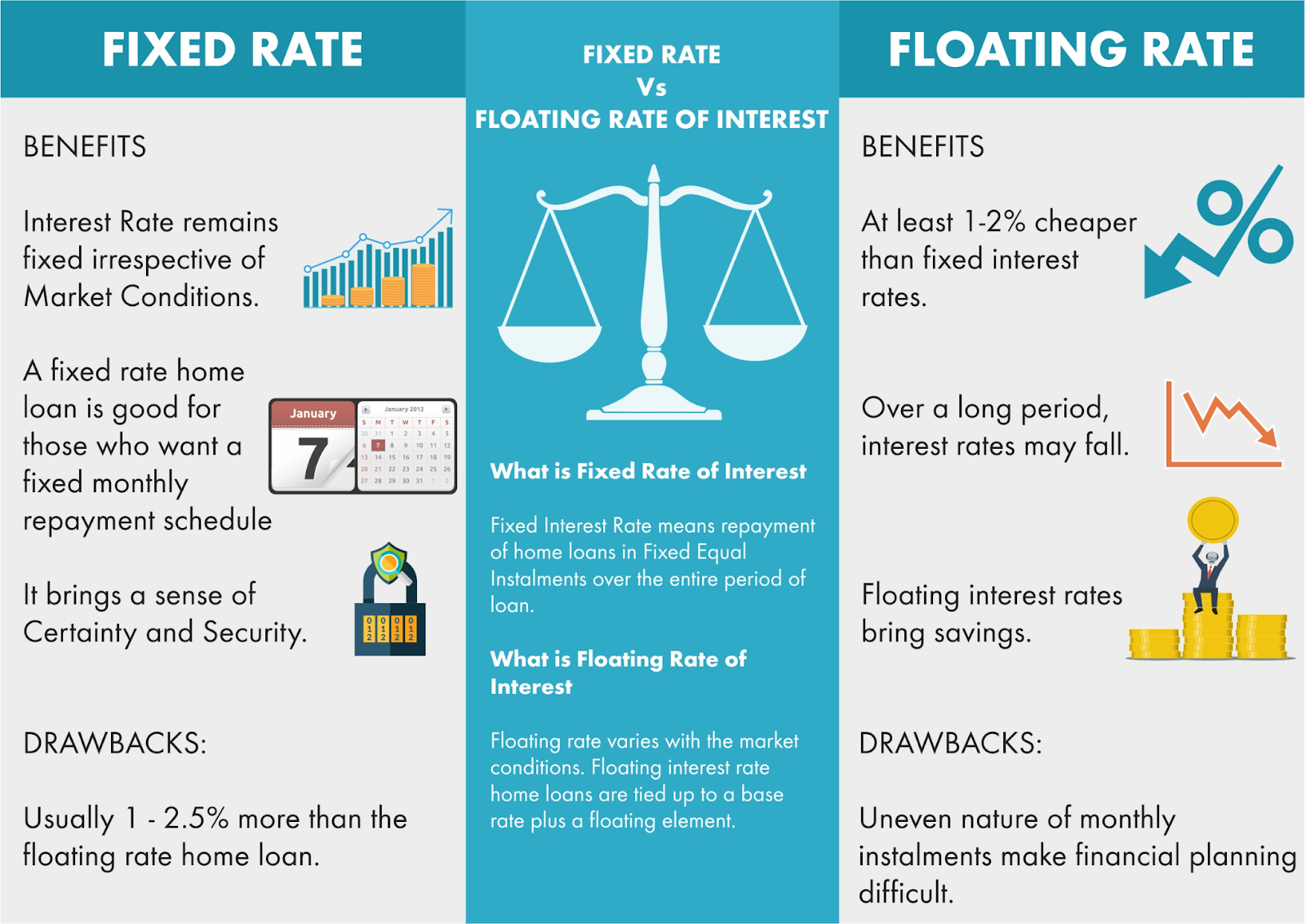

Fixed-Rate Home Loans:

Fixed-rate home loans offer stability and predictability to borrowers. As the name suggests, the interest rate remains unchanged throughout the loan tenure, providing borrowers with a sense of security against fluctuating market conditions. This means that regardless of economic fluctuations or changes in the lending landscape, your monthly payments will remain constant.

Fixed-rate home loans are particularly appealing during periods of high interest rates or economic uncertainty, as they shield borrowers from potential rate hikes. However, it's important to note that fixed-rate loans may come with slightly higher interest rates compared to variable-rate loans, as borrowers pay a premium for the stability they offer.

-

Variable-Rate Home Loans:

In contrast to fixed-rate loans, variable-rate home loans have interest rates that fluctuate based on market dynamics. These loans are typically linked to a benchmark rate, such as the Marginal Cost of Funds Based Lending Rate (MCLR) or the Reserve Bank of India's repo rate.

As these benchmark rates change, so does the interest rate on the loan, resulting in varying monthly payments for borrowers. Variable-rate home loans offer the potential for lower initial interest rates compared to fixed-rate loans, making them an attractive option when interest rates are expected to decrease. However, borrowers must be prepared for the possibility of increased monthly payments if interest rates rise in the future.

-

Home Loan With Floating Interest Rates:

Floating interest rate home loans are a variant of variable-rate loans, where the interest rate fluctuates within a predetermined range. Unlike fixed-rate loans, which offer a constant rate throughout the loan tenure, floating-rate loans provide borrowers with the flexibility to benefit from decreases in interest rates while protecting them from drastic increases.

This type of home loan is particularly suitable for individuals who anticipate interest rates to remain relatively stable or decline over time. Borrowers should carefully review the terms and conditions of floating-rate loans, including the frequency of interest rate adjustments and the extent of fluctuations allowed within the specified range.

-

Home Loan With Hybrid Interest Rates:

Hybrid interest rate home loans combine the features of both fixed and variable-rate loans, offering borrowers the best of both worlds. In this type of loan, the initial period typically features a fixed interest rate, providing borrowers with stability and predictability during the initial years of the loan tenure.

Once the fixed-rate period expires, the loan transitions to a variable interest rate, allowing borrowers to benefit from market fluctuations. Hybrid interest rate loans are ideal for individuals who seek the security of fixed rates in the short term but also wish to capitalize on potential interest rate decreases in the long run. However, borrowers should be aware of any limitations or conditions associated with the transition from fixed to variable rates, such as reset periods and conversion fees.

-

Home Loan With Flexible Repayment Options:

Flexible repayment home loans cater to the diverse financial needs and preferences of borrowers by offering customizable repayment structures. These loans allow borrowers to adjust their EMI (Equated Monthly Installment) amounts or repayment tenures based on changes in their financial circumstances.

For example, borrowers may opt for lower EMIs during the initial years of the loan tenure and gradually increase them as their income grows. Alternatively, borrowers facing temporary financial constraints may choose to defer EMIs or avail of a moratorium period, wherein they temporarily suspend loan repayments.

Flexible repayment options provide borrowers with greater control over their finances and can help mitigate financial stress during unforeseen circumstances. However, borrowers should carefully evaluate the long-term implications of any adjustments to their repayment schedule, including the impact on overall interest costs and loan tenure.

Conclusion:

In conclusion, the journey to homeownership in India is paved with various home loan options, each offering its unique advantages and considerations. Whether you prioritize stability, flexibility, or cost-effectiveness, there's a home loan tailored to suit your needs.

By understanding the intricacies of different home loan types, you can make an informed decision that aligns with your financial goals and aspirations of owning a home. Remember to consult with financial experts and compare multiple loan offers before making a final decision. With the right knowledge and guidance, you can embark on your homeownership journey with confidence and clarity.

0 comments

Log in to leave a comment.

Be the first to comment.